Take a deep breath, pour yourself a fresh cup of coffee, or whatever is your beverage of choice to relax with, start the song (right click and select open in a new tab or window to avoid navigating away from this page), and read the article, “A few reasons to be optimistic about the U.S. economy.” I’m sure you’ll begin to feel much better.

Then, when you’re ready to stop basking in fairytales and return to the real world, ask yourself:

1) If U.S. Healthcare cost increases are slowing due to something other than the economy, how does one explain a global slowdown in healthcare costs? Is the global slowdown also slowing due to the prospect of implementing ObamaCare in 2014? The proposition seems dubious. Further, even if the slowdown is for a reason other than the weak economy, does it really provide a boost to the broader economy when the pace of spending increase is still greater than the pace of increase in U.S. private worker pay?

2) It certainly appears that after six long years the U.S. Housing sector is definitely getting better (fingers crossed; registration required to view link). However, in the “WAHT award-winning” article there seems to be a view the Federal Reserve’s interest rate policy is separate from what the economy does. Said another way, if the housing improvement translates into what is described as “really turns around,” won’t the Federal Reserve raise its “super-low interest rates” to avoid overheating the economy? And why are interest rates still so low? Is it for housing, or for another reason? Concern has already been expressed over maintaining low interest rates in the present economic environment by some Federal Reserve presidents, although those sharing this view are in a minority among voting members this year

Recent comments from Chairman Bernanke address these issues (emphasis added). The first issue is why interest rates are still low:

“If, as the FOMC anticipates, the economic recovery continues at a moderate pace, with unemployment slowly declining and inflation expectations remaining near 2 percent, then long-term interest rates would be expected to rise gradually toward more normal levels over the next several years. This rise would occur as the market's view of the expected date at which the Federal Reserve will begin the removal of policy accommodation draws nearer and then as accommodation is removed. Some normalization of the term premium might also contribute to a rise in long-term rates.”

The key to note here is not a word about the housing market. The Fed’s accommodative policy is principally due to high unemployment levels and, secondarily, a fear of deflation. So, by keeping rates low and policy lax, the Fed hopes to maintain some inflation in the face of significant economic slack.

The second issue is: What happens if the economy begins to strengthen if, say, an improving housing market provides added spark:

“If, as the FOMC anticipates, the economic recovery continues at a moderate pace, with unemployment slowly declining and inflation expectations remaining near 2 percent, then long-term interest rates would be expected to rise gradually toward more normal levels over the next several years. This rise would occur as the market's view of the expected date at which the Federal Reserve will begin the removal of policy accommodation draws nearer and then as accommodation is removed. Some normalization of the term premium might also contribute to a rise in long-term rates.”

Two observations on the quote above: 1) The reason rates are low is because the economy is weak. When the economy isn’t weak interest rates won’t remain low, they’ll increase. Why? Because 2) central banks need to meet their price stability mandates and leaving rates low won’t allow that to happen. So, when interest rates finally begin to increase again, what happens to interest payments on the U.S. debt? I suspect a new crisis unfolds.

3) The WAHT award winner hypothesizes our recent episodes of "genuine malgovernance" were caused by the “extraordinary stresses the recession put on the political system”…. how quaint. I turn to Mark Twain’s (1836 to 1910, RIP) quote: “Suppose you were an idiot, and suppose you were a member of Congress; but I repeat myself.” I’m guessing Mark Twain wasn’t prophesying about today’s federal government but instead lamenting the one of his day. I’m not holding out much hope we’re seeing a sea change on this one.

4) U.S. Corporate profits are strong -- and that’s a good thing -- but it appears one of the reasons they’re strong is due to corporations paying lower wages. This isn’t a shocking result given labor slack. However, U.S. consumers need disposable income if they’re going to buy the things that drive corporate sales that result in corporate profits. But U.S. households have been losing ground on that score for some time; real disposable income is down as well, both in aggregate as well as on a per capita basis. Thus, the current situation doesn’t seem particularly sustainable.

5) Neither Europe nor China appears to be tumbling off an economic cliff...Cómo? While China may not be falling off an economic cliff, it certainly isn’t roaring and substantial risks remain as it navigates from an investment- and export-led economy to a consumer-driven economy. However, characterizing that Europe isn’t falling off an economic cliff makes me wonder what our WAHT award winner is reading about the European economy because it clearly isn’t what I’m reading. While much of the mainstream media likes to proclaim the crisis is over, it seems it doesn’t take long for the crisis pop right back up again, which makes me suspect it never really left in the first place. Informed opinion seems to agree the Euro crisis is far from over too; unemployment conditions, economic data, and recent political events seem to indicate there is little prospect of resolution any time soon.

6) Two other suggestions, that technology will deliver job and wage growth and the U.S. is on the threshold of an "insourcing boom" seem speculative at present.

In fact, one of the mechanisms providing the aforementioned record corporate profits is productivity-enhancing technology -- resulting in lower wages being paid. Frequently the direct pay-off for such technology is worker displacement. I don’t argue against this because such creative destruction (i.e., innovation) is needed for American enterprise to remain globally competitive. I simply highlight that these two points of optimism are somewhat contradictory.

As far as being on the threshold of an “insourcing boom,” I appreciate the quip: “anecdotes aren’t data.” I'm glad for the people of Louisville, Kentucky who are benefiting from General Electric's decision to bring manufacturing jobs back to their Appliance Park facility. But a company making some decisions, even one as big as GE, doesn't mean a new era is upon us. The "tale of the tape" for either technology or insourcing will be if job growth accelerates; so far the jury is out on that score despite February’s favorable employment job growth print.

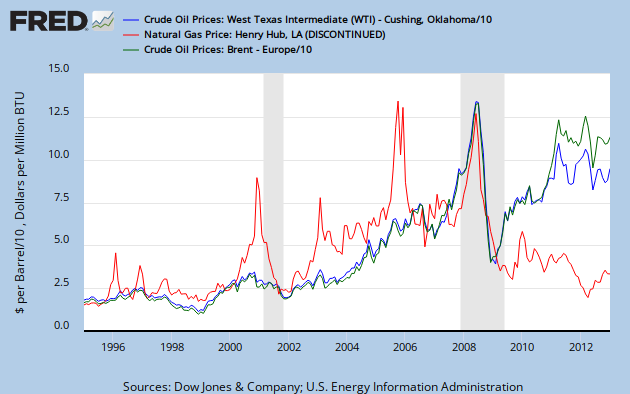

7) The point about natural gas prices is definitely a positive for U.S. growth prospects going forward. I’ll spare readers the pessimism of “malgoverance” finding a way to turn a positive into a negative. After all, this post is about feeling optimistic and earlier it was posited by the WHAT award-winning article the period of “genuine malgoverance” may indeed be behind us. I will, however, point out the inevitable -- but positive, assuming no added regulatory burden -- that natural gas prices will increase. That is because given the recent divergence between crude oil and natural gas prices, consumption will shift away from crude oil and toward natural gas. On a net basis that will result in lower energy costs -- a good thing for the U.S. economy.

8) The final point, that U.S. consumer confidence as measured by Gallup is up from where it was during the recession, is definitely true. But saying that is a bit like (to use a basketball analogy since March Madness is nearly upon us) commenting at 3 minutes into the second half your team is staging a comeback because they’ve narrowed the opponent’s lead by 8 points since halftime. But the lead at halftime was 35 points -- still a long way to go.

The great enemy of the truth is very often not the lie, deliberate, contrived and dishonest, but the myth, persistent, persuasive and unrealistic.

John F. Kennedy

8) The final point, that U.S. consumer confidence as measured by Gallup is up from where it was during the recession, is definitely true. But saying that is a bit like (to use a basketball analogy since March Madness is nearly upon us) commenting at 3 minutes into the second half your team is staging a comeback because they’ve narrowed the opponent’s lead by 8 points since halftime. But the lead at halftime was 35 points -- still a long way to go.

The great enemy of the truth is very often not the lie, deliberate, contrived and dishonest, but the myth, persistent, persuasive and unrealistic.

John F. Kennedy

The result of this deception Is very strange to tell,

For when I fool the people I fear, I fool myself as well!

Selected lyrics from “Whistle a Happy Tune”

Oscar Hammerstein II, lyrist

Selected lyrics from “Whistle a Happy Tune”

Oscar Hammerstein II, lyrist

{kind=link}

{kind=link}